Data is at the heart of our business

We’re entrusted with data on 1.5 billion people and 201 million businesses worldwide. We’ve developed our Global Data Principles and continue to embed this framework to guide how we manage and use data, build products and conduct our business around the world.

Security

Data security is critical. Securing and protecting data against unauthorised access, use, disclosure and loss are key priorities for us.

Accuracy

We will make data as accurate, complete and relevant as possible for the manner in which it is used, always in compliance with legal requirements.

Fairness

We collect and use data fairly and for legitimate purposes derived from the responsible use of data for individuals, businesses and clients.

Transparency

We are open and transparent about the types of data we collect, where we get it, how it is used and where it is shared.

Inclusion

We seek to improve financial health and inclusion for all through the innovative use of relevant data to help individuals improve their financial lives.

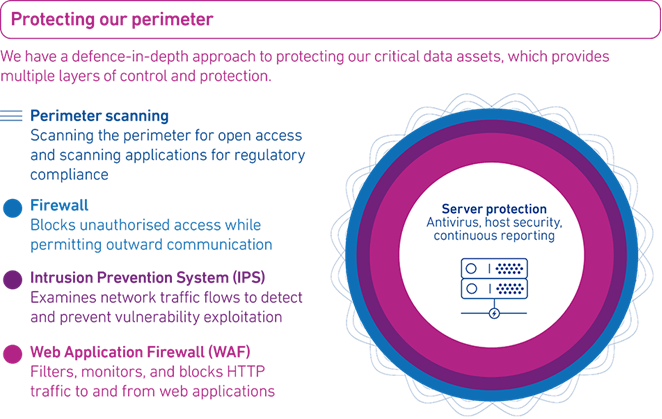

Security

The loss or inappropriate use of data and systems could result in material loss of business, substantial legal liability, regulatory enforcement actions and significant harm to our reputation.

Security comes first at Experian. We continually enhance and invest in our security infrastructure, practices and culture across the business. We have specialist teams, state-of-the-art technology and rigorous due-diligence procedures to deal with potential cyber security threats.

Our security approach has three tiers: applying tools and processes to prevent threats from entering our environment, detecting if a threat enters our environment, and mitigating any threats by minimising the potential for information to be extracted from our environment. Threat-informed defence helps us shape, assess, prioritise and measure the effectiveness of our approach.

Accuracy

Accurate credit reports enable lenders to give people fairer access to credit and essential services to improve their lives. Any inaccuracies in credit reports — and the data they’re built on — can cause problems for consumers and potentially deny them fair access to credit and services.

We understand how important this issue is for consumers, and accuracy is one of our Global Data Principles that guide our approach wherever we operate. Data accuracy principles are also being written into data protection regulations in many countries.

We’re committed to making data as accurate, complete and relevant as possible for the way it’s used, always in compliance with legal requirements. We constantly strive to improve the accuracy of our data in a competitive market to ensure our clients can always rely on it to make appropriate decisions.

We have strict processes for data accuracy — from sourcing accurate data in the first place to monitoring and improving accuracy over time and resolving reported inaccuracies or information queried by consumers. Our focus is on the timeliness, accuracy and completeness of the data we hold and the reports we provide to our clients.

Fairness

We’re committed to collecting and using data fairly and for legitimate purposes and complying with regulations on data lifecycle and retention in the markets in which we operate. We carefully balance privacy expectations with the social and economic benefits derived from the responsible use of data for individuals, businesses and clients.

Our privacy policies vary in each country or region to comply with local regulatory requirements. Underlying these policies is our commitment to provide consumers with notice, choice and education about the use of personal information. Educated consumers are better equipped to be effective, successful participants in a world that increasingly relies on the exchange of information to deliver relevant products and services efficiently.

Lenders need access to accurate information about people’s financial profiles from Experian or other credit bureaux. Such information is integral to an efficient and competitive credit ecosystem that provides innovative products which enable consumers to get the most out of their data, contributes to economic growth and supports a stable consumer banking system.

Transparency

We strive to be open and transparent about the types of data we collect from consumers and third parties, where we get it, how it’s used and where it’s shared. Where appropriate, we provide individuals with access to the data we collect about them and give them the ability to correct, restrict and delete data.

Data transparency not only empowers consumers, it also benefits our business. For example, our marketing services are more effective for our clients when more people understand their ability to set their marketing preferences, as this means fewer people receive unwanted marketing to which they would not be receptive.

Inclusion

We enhance financial inclusion by using data to create insights that help lenders offer fairer access to credit to more people. Our aim is to help more people get better access to credit by sharing relevant data with lending organisations, including adding alternative sources of data, such as positive data about on-time payments of utility bills and subscription services.

Read our 2023 Improving Financial Health Report for more on our use of data to improve financial inclusion and financial health.