Costa Mesa, Calif., June 25, 2015 — Today, Experian’s global Fraud and Identity business released its analysis of client transaction data from the 2014 holiday season, showing an 80 percent reduction in the number of manual reviews among online merchants using the company’s fraud and identity products and services compared with the industry average. These results and other observations indicate that a customer-centric approach to fraud prevention would be more effective for many online merchants, leading the company to recommend five best practices for online merchants preparing for the 2015 holiday season.

Experian fraud improvements over industry average

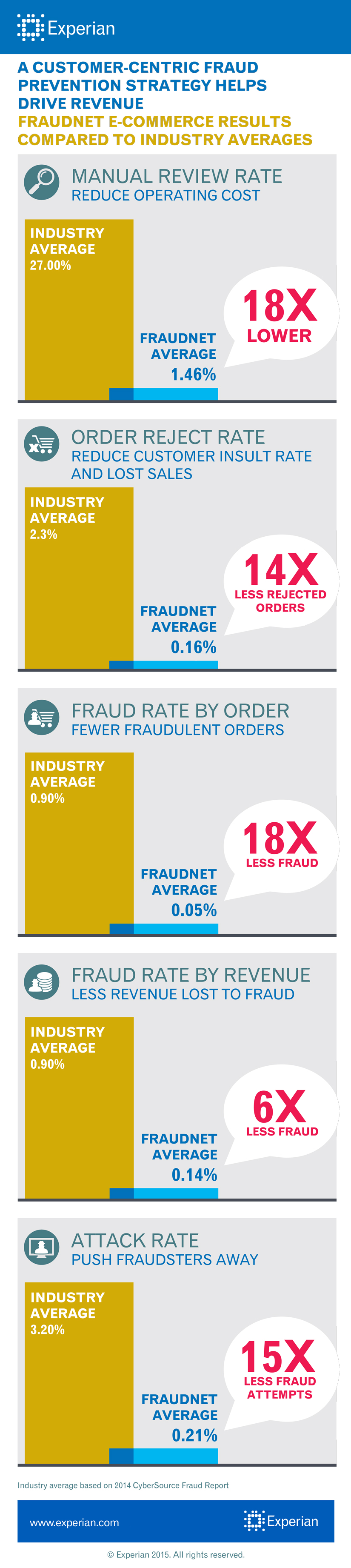

Pulled for manual review: 18x fewer orders pulled for manual review

Order reject rate: 14x fewer rejected orders

Attack rate: 15x fewer fraud attempts

Source: Data is based on Cybersource 2014 Fraud Report and Experian analysis of client transactions. The industry average for orders pulled for manual review is 5 percent to 30 percent or higher, depending on the size of the organization.

[View our Customer Centric Fraud Prevention Strategy infographic]

Experian’s holiday fraud data highlighted the performance delta between the company’s technology and alternative approaches. Many merchants, for example, will loosen their fraud rules to process more orders during peak periods. To compensate for the increased risk of fraud caused by this approach, more manual reviews were conducted. This is a counterproductive approach that drives up operating costs and increases customer friction. Despite the increase in manual reviews, undetected fraud can occur and good revenue can be left on the table.

“Good fraud detection should be about more than preventing loss. It should increase revenue by allowing more good customers through and providing a hassle-free shopping experience, especially during the critical holiday shopping season,” said Steve Platt, Global EVP, Fraud and Identity, Experian. “To help our clients with this, we combine insights derived from device intelligence and digital behavior, with the contextual data about the event itself (e.g., transaction, application, login, etc.). We analyze millions of transactions per day, evaluate risk in real time and deliver responses in mere milliseconds. With this approach, our clients are catching more fraud and reducing customer friction, leading to fewer manual reviews and lower operational costs. It’s a win-win-win.”

For one U.S. multichannel retail client, this “win” translated into a 95 percent detection rate (amount of fraud caught) valued at $17.3 million during the fourth quarter alone. This is just one example of how applying the following recommended best practices can help clients reduce fraud and drive top-line growth.

Best fraud-prevention practices for the holidays

With the 2015 holiday shopping season less than five months away, now is the time for merchants to prepare to effectively protect themselves and their customers during the busiest time of the year. Experian® shares five fraud-prevention best practices for a stronger 2015 holiday sales cycle:

•Avoid one-size-fits-all approaches — Many online merchants make a general temporary adjustment to loosen fraud-prevention rules, supplementing with additional manual reviews to accommodate the increased holiday volume. Not only does this increase operational costs for the business, but it also translates to an insult rate (falsely identifying good customers) of 29 percent to address a 0.9 percent problem. This is a significant imbalance. By leveraging the right fraud-prevention measures at the right time, you’ll see increased and sustainable top-line growth.

•Make your customer data work for you across the business — While many risk teams already use internal customer data to improve fraud detection, the explosion of channels and devices means there are other data sets across the enterprise that can be leveraged effectively to maintain visibility and authenticate identities across the digital ecosystem. Further, by establishing and maintaining a single, persistent customer view, companies benefit from additional, actionable insights throughout the customer journey. According to Experian Marketing Services’ 2015 Digital Marketer Report, 89 percent of marketers globally say that they have trouble achieving a single customer view. By using technology to link data sets and identities together — like customer loyalty data with customer transactional data, social and digital behavior, demographics and more — merchants are getting a clearer picture of who their customers are. In addition, they have a better understanding of how those customers engage across channels. It is also critical to understand that the amount of data alone is not the answer; the insights and intelligence gleaned from or applied to that data must be considered as well.

•Bring fraud and marketing efforts together — Although this is not an obvious combination at first glance, this relationship can be one of the most powerful in the enterprise. Just last year, a survey by Experian Marketing Services reported that 80 percent of marketers planned to run cross-channel marketing campaigns in 2014. More channels, more campaigns and increased volume mean new challenges for fraud-risk managers. Together, fraud and marketing teams can help the top line and the bottom line by preventing bad transactions without impacting the customer experience. The past often can tell a lot about the future. These groups should jointly review past holiday performance in terms of both top-line growth (i.e., successful campaigns) and successful risk strategies that complement those growth objectives and use the insight to form future strategies.

•Establish a dedicated team responsible for the customer experience — Several of our financial services clients are reporting notable success with digital groups. These teams are responsible for bringing together marketing, risk and consumer experience experts to create and maintain a directional and strategic customer purview across channels. Formalizing the sharing of data, processes and best practices among these traditionally siloed departments is a way to process more customers while reviewing fewer transactions, catching more fraud and providing a hassle-free customer experience.

•Stay ahead of evolving market conditions — There are some things that are out of retailers’ control, such as the impending October 2015 EMV rollout in the United States. While most point-of-sale transactions will be vastly safer and more secure as a result of the rollout, we have seen card-not-present fraud rise in Europe, where EMV already is in place. This is because criminals will focus their energies on the fraud they can still perpetrate. We also have the proliferation of personalized mobile transactions. While this technology aids in ensuring a seamless customer experience, personal and/or financial information now is being exchanged at an increasing rate and exposing businesses to new fraud risks. Being aware and having a plan to react quickly to the ever-changing fraud landscape can significantly increase the chances of thwarting criminals and keeping businesses safe.

Listen to a recording of our 2015 Holiday Fraud webinar to learn how your business can prepare its fraud strategy for this season.

Contact:

Matt Tatham

Experian Public Relations

1 212 380 2939

matt.tatham@experian.com

About Experian

We are the leading global information services company, providing data and analytical tools to our clients around the world. We help businesses to manage credit risk, prevent fraud, target marketing offers and automate decision making. We also help people to check their credit report and credit score, and protect against identity theft. In 2014, we were named by Forbes magazine as one of the “World’s Most Innovative Companies.”

We employ approximately 17,000 people in 39 countries and our corporate headquarters are in Dublin, Ireland, with operational headquarters in Nottingham, UK; California, US; and São Paulo, Brazil.

Experian plc is listed on the London Stock Exchange (EXPN) and is a constituent of the FTSE 100 index. Total revenue for the year ended March 31, 2015, was US$4.8 billion.

To find out more about our company, please visit http://www.experianplc.com or watch our documentary, “Inside Experian.”

{kind=link}